Vertex: Great Company, Harder Stock Question

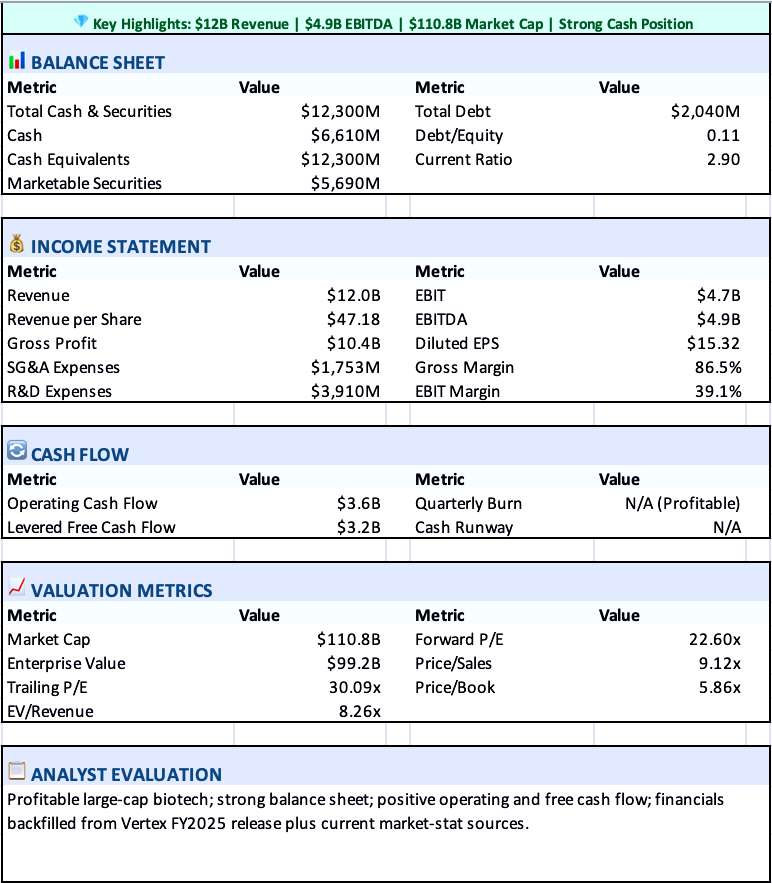

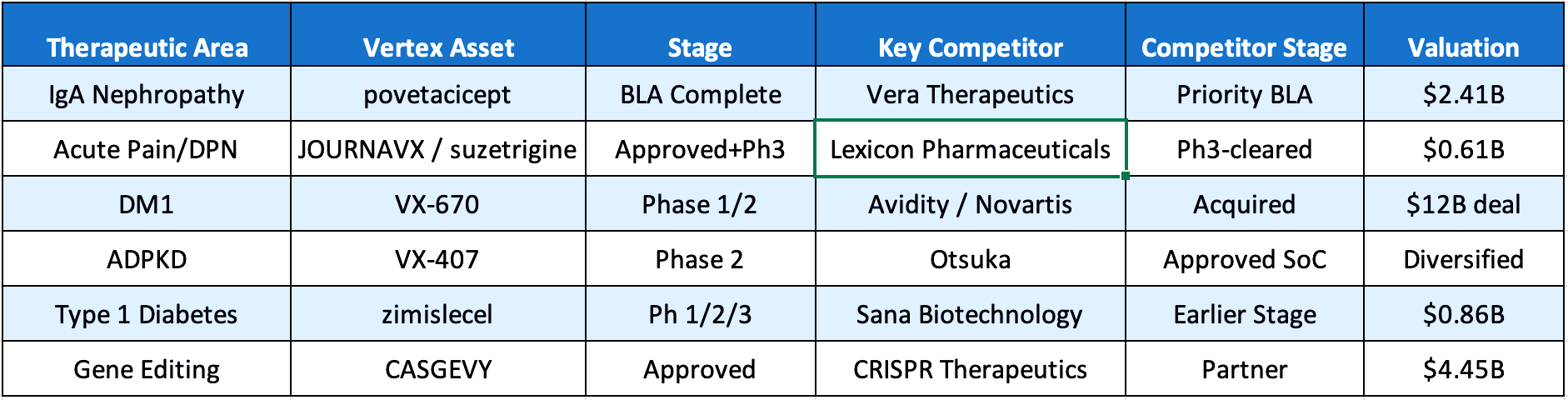

Vertex Pharmaceuticals (VRTX) still looks like one of biotech’s highest-quality compounders, but the stock is no longer just a CF story. The real debate is how much of the next wave—povetacicept in IgAN, JOURNAVX in pain, and selected renal / neuromuscular optionality—is already priced into a $110B+ market cap.

The core CF franchise continues to throw off cash and gained another boost from April’s U.S. label expansions, while the non-CF pipeline is now large enough that investors need to separate durable base-business value from scenario-driven upside.

In other words, the right question on Vertex today is not whether it is a strong company, but whether the market is already paying too much for the next layer of growth.

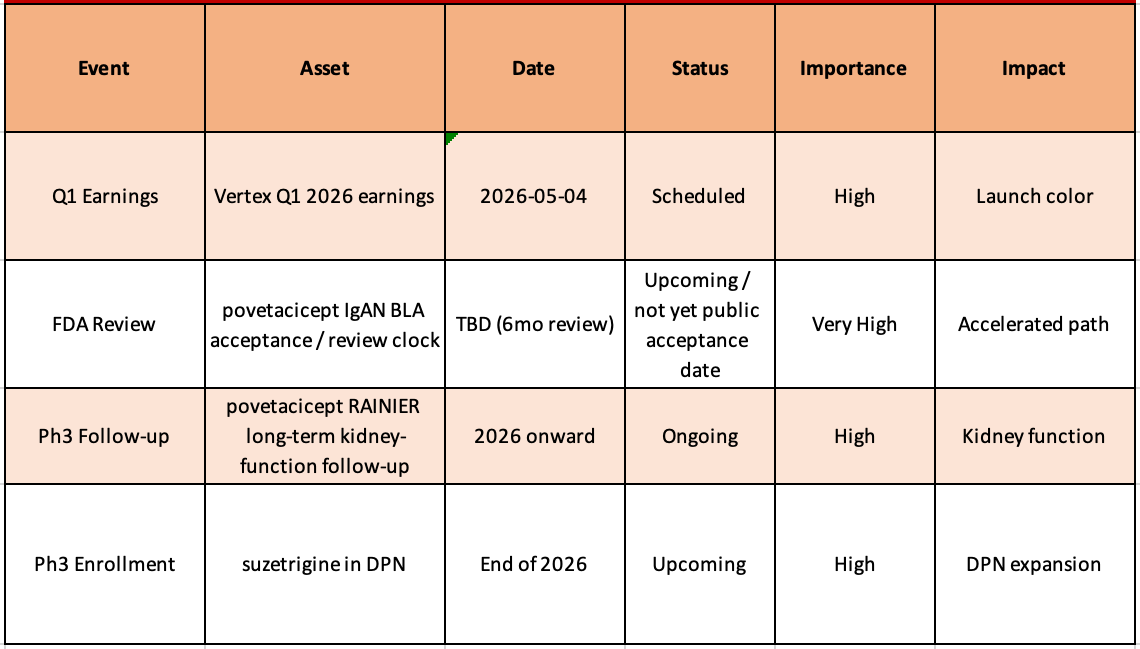

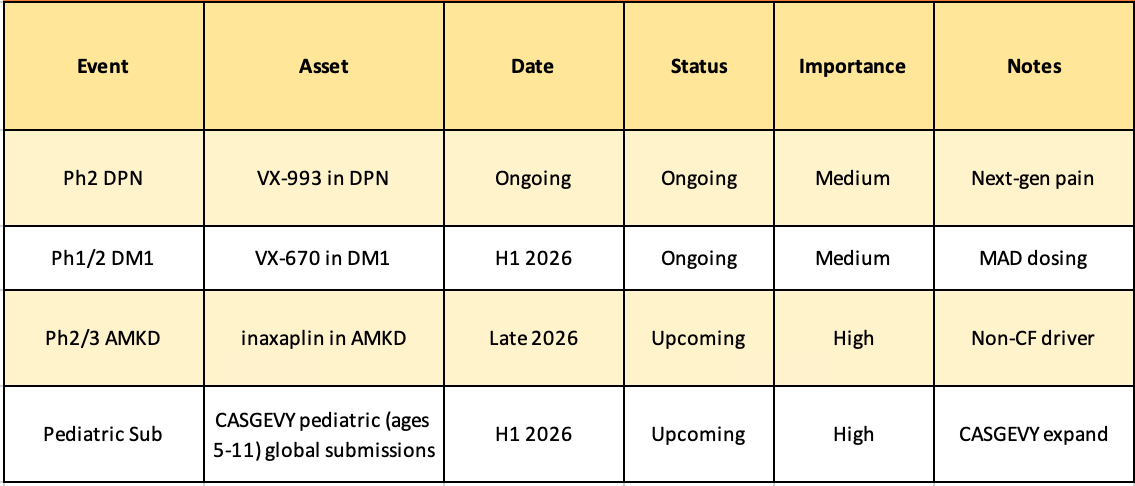

Upcoming Catalysts (High Priority-Red, Medium Priority-Orange)

All in all, the CF engine is still elite, but the real valuation debate has shifted to how much IgAN, pain, renal, and cell-therapy optionality is already embedded in today’s stock price.